* The preview only shows a few pages of manuals at random. You can get the complete content by filling out the form below.

Description

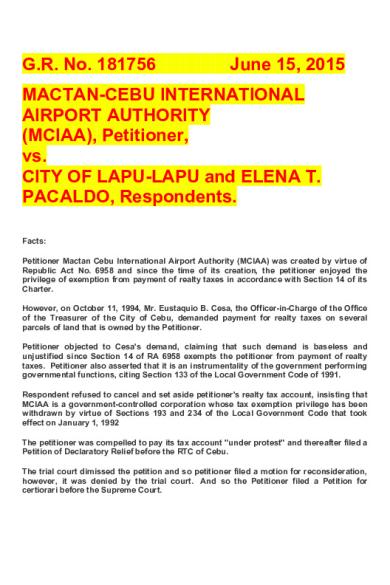

G.R. No. 181756 June 15, 2015 MACTAN-CEBU INTERNATIONAL AIRPORT AUTHORITY (MCIAA), Petitioner, vs. CITY OF LAPU-LAPU and ELENA T. PACALDO, Respondents. Facts: Petitioner Mactan Cebu International Airport Authority (MCIAA) was created by virtue of Republic Act No. 6958 and since the time of its creation, the petitioner enjoyed the privilege of exemption from payment of realty taxes in accordance with Section 14 of its Charter. However, on October 11, 1994, Mr. Eustaquio B. Cesa, the Officer-in-Charge of the Office of the Treasurer of the City of Cebu, demanded payment for realty taxes on several parcels of land that is owned by the Petitioner. Petitioner objected to Cesa's demand, claiming that such demand is baseless and unjustified since Section 14 of RA 6958 exempts the petitioner from payment of realty taxes. Petitioner also asserted that it is an instrumentality of the government performing governmental functions, citing Section 133 of the Local Government Code of 1991. Respondent refused to cancel and set aside petitioner's realty tax account, insisting that MCIAA is a government-controlled corporation whose tax exemption privilege has been withdrawn by virtue of Sections 193 and 234 of the Local Government Code that took effect on January 1, 1992 The petitioner was compelled to pay its tax account "under protest" and thereafter filed a Petition of Declaratory Relief before the RTC of Cebu. The trial court dimissed the petition and so petitioner filed a motion for reconsideration, however, it was denied by the trial court. And so the Petitioner filed a Petition for certiorari before the Supreme Court.

Issue: Whether or not MCIAA is exempted from paying its realty taxes?

Ruling: No. The SC held that, tax exemptions or incentives granted to or presently enjoyed by natural or juridical persons, including government-owned and controlled corporations, Section 193 of the LGC prescribes the general rule, viz., they are withdrawn upon the effectivity of LGC, except upon the effectivity of the LGC, except those granted to local water districts, cooperatives duly registered under RA No. 6938, non stock and non-profit hospitals and educational institutions, and unless otherwise provided in the LGC. Since the last paragraph of Section 234 unequivocally withdrew, upon the effectivity of the LGC, exemptions from real property taxes granted to natural or juridical persons, including government-owned corporation, except as provided in the said section, and the petitioner is, undoubtedly, a government-owned corporation, it necessarily follows that its exemption from such tax granted it in Section 14 of its Charter, RA No. 6938, has been withdrawn. In short, the petitioner can no longer invoke the general rule in Section 133. Also, If Section 234(a) intended to extend the exception therein to the withdrawal of the exemption from payment of real property taxes under the last sentence of the said section to the agencies and instrumentalities of the National Government mentioned in Section 133(o), then it should have restated the wording of the latter. Yet, it did not. Moreover, the Congress did not wish to expand the scope of the exemption is Section 234(a) to include real property owned by other instrumentalities or agencies of the government including government-owned and controlled corporations is further borne out by the fact that the source of this exemption is Section 40(a) of P.D. No. 646, otherwise known as the Real Property Tax Code.

MACTAN-CEBU INTERNATIONAL AIRPORT AUTHORITY (MCIAA) V. CITY OF LAPU-LAPU AND PACALDO, G.R. NO. 181756, [JUNE 15, 2015] FACTS: Petitioner Mactan-Cebu International Airport Authority (MCIAA) was created by Congress on July 31, 1990 under Republic Act No. 6958 to “undertake the economical, efficient and effective control, management and supervision of the Mactan International Airport in the Province of Cebu and the Lahug Airport in Cebu City . . . and such other airports as may be established in the Province of Cebu.” It is represented in this case by the Office of the Solicitor General. Respondent City of Lapu-Lapu is a local government unit and political subdivision, created and existing under its own charter with capacity to sue and be sued. Respondent Elena T. Pacaldo was impleaded in her capacity as the City Treasurer of respondent City. aScITE Upon its creation, petitioner enjoyed exemption from realty taxes under the following provision of Republic Act No. 6958: Section 14. Tax Exemptions. — The Authority shall be exempt from realty taxes imposed by the National Government or any of its political subdivisions, agencies and instrumentalities: Provided, That no tax exemption herein granted shall extend to any subsidiary which may be organized by the Authority. On September 11, 1996, however, this Court rendered a decision in Mactan-Cebu International Airport Authority v. Marcos (the 1996 MCIAA case) declaring that upon the effectivity of Republic Act No. 7160 (The Local Government Code of 1991),petitioner was no longer exempt from real estate taxes. The Court held: Since the last paragraph of Section 234 unequivocally withdrew, upon the effectivity of the LGC,exemptions from payment of real property taxes granted to natural or juridical persons, including government-owned or controlled corporations, except as provided in the said section, and the petitioner is, undoubtedly, a government-owned corporation, it necessarily follows that its exemption from such tax granted it in Section 14 of its Charter, R.A. No. 6958, has been withdrawn. . . . .

On January 7, 1997, respondent City issued to petitioner a Statement of Real Estate Tax assessing the lots comprising the Mactan International Airport in the amount of P162,058,959.52. Petitioner complained that there were discrepancies in said Statement of Real Estate Tax as follows: (a) [T]he statement included lots and buildings not found in the inventory of petitioner’s real properties; (b) [S]ome of the lots were covered by two separate tax declarations which resulted in double assessment; (c) [There were] double entries pertaining to the same lots; and (d) [T]he statement included lots utilized exclusively for governmental purposes. Respondent City amended its billing and sent a new Statement of Real Estate Tax to petitioner in the amount of P151,376,134.66. Petitioner averred that this amount covered real estate taxes on the lots utilized solely and exclusively for public or governmental purposes such as the airfield, runway and taxiway, and the lots on which they are situated. Petitioner paid respondent City the amount of four million pesos (P4,000,000.00) monthly, which was later increased to six million pesos (P6,000,000.00) monthly. As of December 2003, petitioner had paid respondent City a total of P275,728,313.36.S Respondent City Treasurer Elena T. Pacaldo sent petitioner a Statement of Real Property Tax Balances up to the year 2002 reflecting the amount of P246,395,477.20. Petitioner claimed that the statement again included the lots utilized solely and exclusively for public purpose such as the airfield, runway, and taxiway and the lots on which these are built. Respondent Pacaldo then issued Notices of Levy on 18 sets of real properties of petitioner. Petitioner filed a petition for prohibition with the Regional Trial Court (RTC) of LapuLapu City with prayer for the issuance of a temporary restraining order (TRO) and/or a writ of preliminary injunction, docketed as SCA No. 6056-L. Branch 53 of RTC LapuLapu City then issued a 72-hour TRO. The petition for prohibition sought to enjoin respondent City from issuing a warrant of levy against petitioner’s properties and from selling them at public auction for delinquency in realty tax obligations. The petition likewise prayed for a declaration that the airport terminal building, the airfield, runway, taxiway and the lots on which they are situated are exempted from real estate taxes after due hearing. Petitioner based its claim of exemption on DOJ Opinion No. 50.

The RTC issued an Order denying the motion for extension of the TRO. Thus, on December 10, 2003, respondent City auctioned 27 of petitioner’s properties. As there was no interested bidder who participated in the auction sale, respondent City forfeited and purchased said properties. The corresponding Certificates of Sale of Delinquent Property were issued to respondent City. Petitioner claimed before the RTC that it had discovered that respondent City did not pass any ordinance authorizing the collection of real property tax, a tax for the special education fund (SEF), and a penalty interest for its nonpayment. Petitioner argued that without the corresponding tax ordinances, respondent City could not impose and collect real property tax, an additional tax for the SEF, and penalty interest from petitioner. ISSUE: WON MCIAA IS SUBJECT TO LOCAL AND REAL PROPERTY TAXATION. HELD: NO. To summarize, MIAA is not a government-owned or controlled corporation under Section 2(13) of the Introductory Provisions of the Administrative Code because it is not organized as a stock or non-stock corporation. Neither is MIAA a governmentowned or controlled corporation under Section 16, Article XII of the1987 Constitution because MIAA is not required to meet the test of economic viability. MIAA is a government instrumentality vested with corporate powers and performing essential public services pursuant to Section 2(10) of the Introductory Provisions of the Administrative Code. As a government instrumentality, MIAA is not subject to any kind of tax by local governments under Section 133(o) of the Local Government Code. The exception to the exemption in Section 234(a) does not apply to MIAA because MIAA is not a taxable entity under the Local Government Code. Such exception applies only if the beneficial use of real property owned by the Republic is given to a taxable entity. Finally, the Airport Lands and Buildings of MIAA are properties devoted to public use and thus are properties of public dominion. Properties of public dominion are owned by the State or the Republic. . The term “ports . . . constructed by the State” includes airports and seaports. The Airport Lands and Buildings of MIAA are intended for public use, and at the very least intended for public service. Whether intended for public use or public service, the Airport Lands and Buildings are properties of public dominion. As properties of public dominion, the Airport Lands and Buildings are owned by the Republic and thus exempt from real estate tax under Section 234(a) of the Local Government Code. Under Section 2(10) and (13) of the Introductory Provisions of the Administrative Code, which governs the legal relation and status of government units, agencies and offices within the entire government machinery, MIAA is a government instrumentality and not a government-owned or controlled corporation. Under Section 133(o) of the Local

Government Code, MIAA as a government instrumentality is not a taxable person because it is not subject to “[t]axes, fees or charges of any kind” by local governments. The only exception is when MIAA leases its real property to a “taxable person” as provided in Section 234(a) of the Local Government Code, in which case the specific real property leased becomes subject to real estate tax. Thus, only portions of the Airport Lands and Buildings leased to taxable persons like private parties are subject to real estate tax by the City of Parañaque. Under Article 420 of the Civil Code, the Airport Lands and Buildings of MIAA, being devoted to public use, are properties of public dominion and thus owned by the State or the Republic of the Philippines. Article 420 specifically mentions “ports . . . constructed by the State,” which includes public airports and seaports, as properties of public dominion and owned by the Republic. As properties of public dominion owned by the Republic, there is no doubt whatsoever that the Airport Lands and Buildings are expressly exempt from real estate tax under Section 234(a) of the Local Government Code. This Court has also repeatedly ruled that properties of public dominion are not subject to execution or foreclosure sale.